Sustainability Reporting Standards in India: 2022

Share

Copy Url

Share

Copy Url

What is Sustainability Reporting?

Sustainability reporting helps companies report and publish their performance and impact metrics across a range of Environment, Social, and Governance (ESG) parameters. The idea behind it is to nudge companies, allowing them to be transparent about their risks and opportunities.

Why is Sustainability Reporting Gaining Traction?

Only one-fifth of 586 companies in India assessed published sustainability reports in 2021. Compared to last year, 12 new companies have made these disclosures for the first time, according to a report by CRISIL. Investors and stakeholders prioritize companies that have ESG ambitions. This elbows companies to clearly communicate their roadmap towards achieving their sustainability goals.

Narrowing in on Standards and Frameworks

In the first step, decide how you want to report on your sustainability measures. Frameworks are broad guidelines that do not impose precise requirements for reporting. Standards or standardization are well-defined. It is expected that these guidelines are strictly followed.

Simply put, frameworks guide you while standards tell you what to report.

Five Widely Adopted Types of Reporting Standards

The following are the 5 that are most widely adopted.

1. Global Reporting Initiative (GRI)

74 out of 498 reporting organizations in India follow the GRI standards.

“Of the world's largest 250 corporations, 93% report on their sustainability performance and 82% of these use GRI Standards to do so.” (GRI at a Glance).

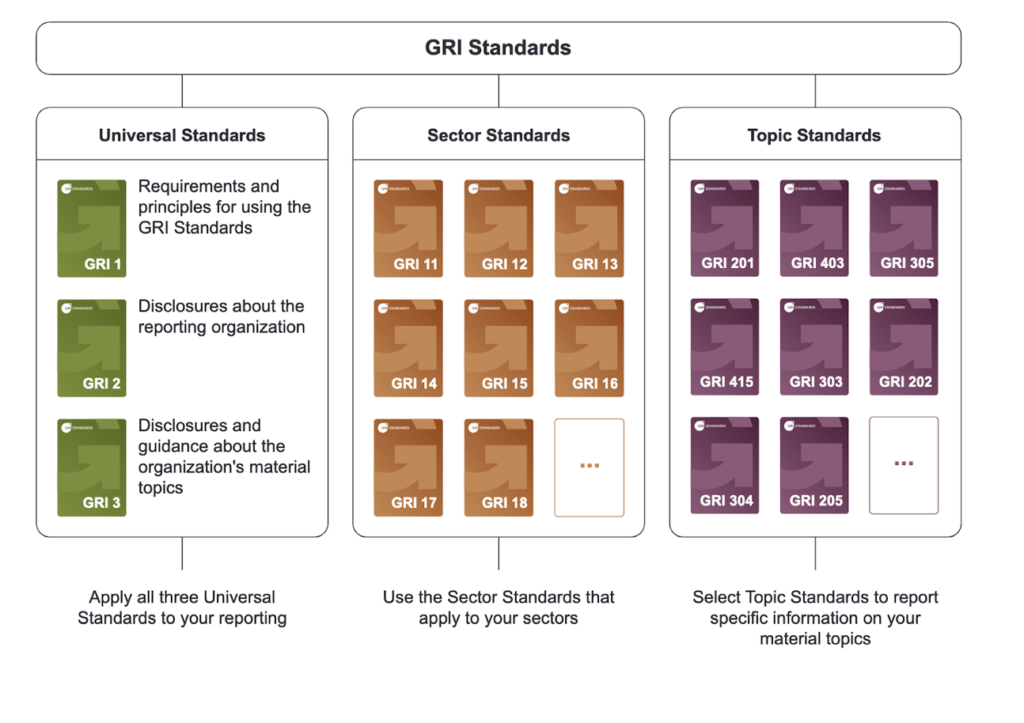

GRI standards are of three types:

a. Universal Standards

GRI 101: Foundation - Implementing GRI Foundation standards is the starting point for all organizations. It introduces the system of GRI and explains how they are to be used. It includes requirements for preparing a sustainability report and describes how the GRI standards should be referenced.

GRI 102: General Disclosures - Organisations are required to submit information on their reporting practices, activities, workers, governance, strategy, policies and practices, and stakeholder engagement. With this information, one can gain a better understanding of the scale and profile of organizations.

GRI 103: Material Topics - The purpose of this set is to ease the efficiency and productivity of GRI reporting. It guides companies on how to identify material topics and disclosures about how the organization identifies material topics and manages each material topic.

b. Topic-specific Standards

Topic standards specify how information should be disclosed. Examples include standards on waste, occupational health and safety, and tax.

GRI 200: Economic Topics - As defined by GRI, GRI 200 comprises 6 categories: economic performance, market presence, indirect economic impacts, procurement practices, anti-corruption, and anti-competitive behavior.

GRI 300: Environmental Topics - Environmental sustainability refers to an organization's effects on living and non-living systems, such as land, air, water, and ecosystems, as described by the GRI standards. The 8 reporting requirements under this series include materials, energy, water, biodiversity, emissions, effluents and waste, environmental compliance, and supplier environmental assessment.

GRI 400: Social Topics - Reporting requirements under this series include employment, labor/ management relations, occupational health and safety, training and education, diversity and equal opportunity, non-discrimination, freedom of association and collective bargaining, child labor, forced or compulsory labor, security practices, rights of indigenous peoples, human rights assessment, local communities, supplier social assessment, public policy, customer health safety, marketing and labeling, customer privacy, and socio-economic compliance.

c. Sector Standards

The purpose of Sector Standards is to enhance transparency and accountability. There are 4 priority groups under the Sector Standards

- Basic materials and needs

- Industrial

- Transport, infrastructure, and tourism

- Other services and light manufacturing

Oil and gas, coal, agriculture, aquaculture, and fishing are the first sectors prioritized under the Sector Program based on their significant environmental, social, and economic impacts.

2. Sustainability Accounting Standards Board (SASB)

In SASB's approach, industries are first categorized by sectors and then given specific sustainability accounting criteria based on the industry's nuances. Materiality assessment is done using the SASB Materiality Map, which depicts the complete set of 77 industry standards (aligned to the Sustainable Industry Classification System, or SICS) including specific industries within Finance, Food & Beverage, Healthcare, Transportation, and more. There is no specific reporting period, but this framework may be complemented by other organizational disclosures. The standards address sustainability-related risks and opportunities reasonably likely to affect an organization's financial condition, operating performance, or risk profile.

3. Carbon Disclosure Project (CDP)

CDP is a global non-profit organization that helps and motivates companies and governments using capital markets and corporate procurement to disclose their environmental impacts and to reduce greenhouse gas emissions, safeguard water resources and protect forests. In 2021, more than 590 investors with over US$110 trillion in assets requested companies to disclose through CDP.

4. Value Reporting Foundation (VRF)

The International Integrated Reporting Council (IIRC) and SASB announced their intention to merge in November 2020 to form the Value Reporting Foundation (VRF). VRF is a global non-profit that offers a comprehensive suite of resources to help businesses and investors better understand enterprise value. SASB Standards, Integrated Thinking Principles, and Integrated Reporting Framework can be used separately or together, depending on business needs. The Integrated Thinking Principles guide Board and Management planning and decision-making. SASB Standards are a powerful tool to inform investor decision-making when embedded in investment tools and processes. In business activities, the VRF refers to its 'capitals' as the broad range of resources and relationships it uses and affects.

The VRF recognizes six distinct but interrelated capitals:

- Financial

- Manufactured

- Natural

- Human

- Intellectual

- Social and Relationships

5. Sustainable Development Goals (SDGs)

80% of the top 100 Indian companies for sustainability and Corporate Social Responsibilities (CSR) in 2021 incorporated Sustainable Development Goals (SDGs) in their responsible business actions. To align with the SDGs, it is necessary not only to understand the SDG framework but also many industry-specific standards. The UN SDGs consist of 17 goals and 169 targets with 230 agreed-upon indicators. The 17 SDGs are:

- No Poverty

- Zero Hunger

- Good Health and Well-being

- Quality Education

- Gender Equality

- Clean Water and Sanitation

- Affordable and Clean Energy

- Decent Work and Economic Growth

- Industry, Innovation, and Infrastructure

- Reduced Inequality

- Sustainable Cities and Communities

- Responsible Consumption and Production

- Climate Action

- Life Below Water

- Life on Land

- Peace and Justice Strong Institutions

- Partnerships to achieve the Goal

6. Science-Based Targets

Science-based targets provide a defined pathway for companies to reduce their greenhouse gas (GHG) emissions, thus mitigating the impact of climate change and future-proofing business growth.

Targets are considered ‘science-based’ if they are in line with what the latest climate science deems necessary to meet the goals of the Paris Agreement – limiting global warming to well below 2°C above pre-industrial levels and pursuing efforts to limit warming to 1.5°C.

As of September 2020, 989 companies and 58 financial institutions have publicly joined the SBTi, among which 467 companies have had their targets officially approved.

Looking Ahead

The progress of sustainability reporting in India is slow, but a significant and sound start has been made. Is sustainability reporting going to continue to evolve as the landscape changes?

Report Yak has a specialized advisory team, content developers, and designers who specifically cater to generating Sustainability Reports for corporates and businesses across the globe. To create your Sustainability Report with us, head here.

Related Posts

-

How To Adopt BRSR Guidelines For Success

Oct 15, 2025Share

Copy Url

Copy Url

GRI Sustainability Taxonomy: Learn How to Turn Data Into Advantage

Jul 1, 2025Share

Copy Url

Latest GRI Updates – What Companies Need to Know

Jun 10, 2025Share

Copy Url